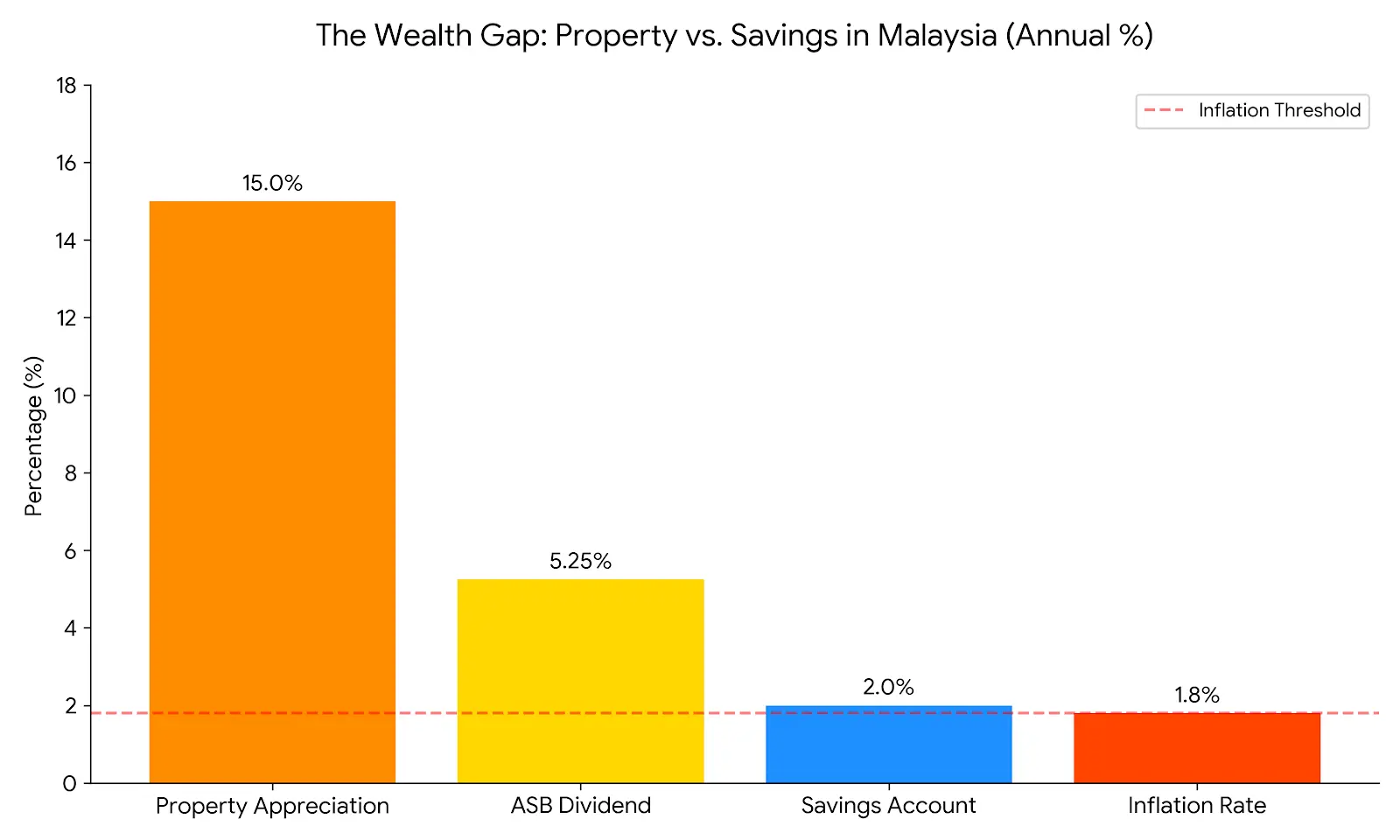

Stop saving for poverty.

Start investing in property

for freedom.

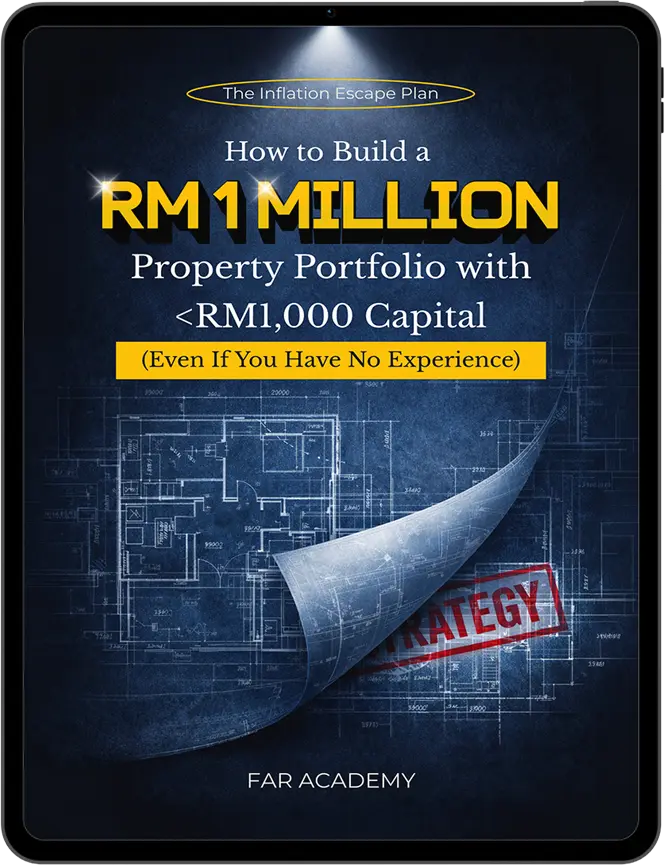

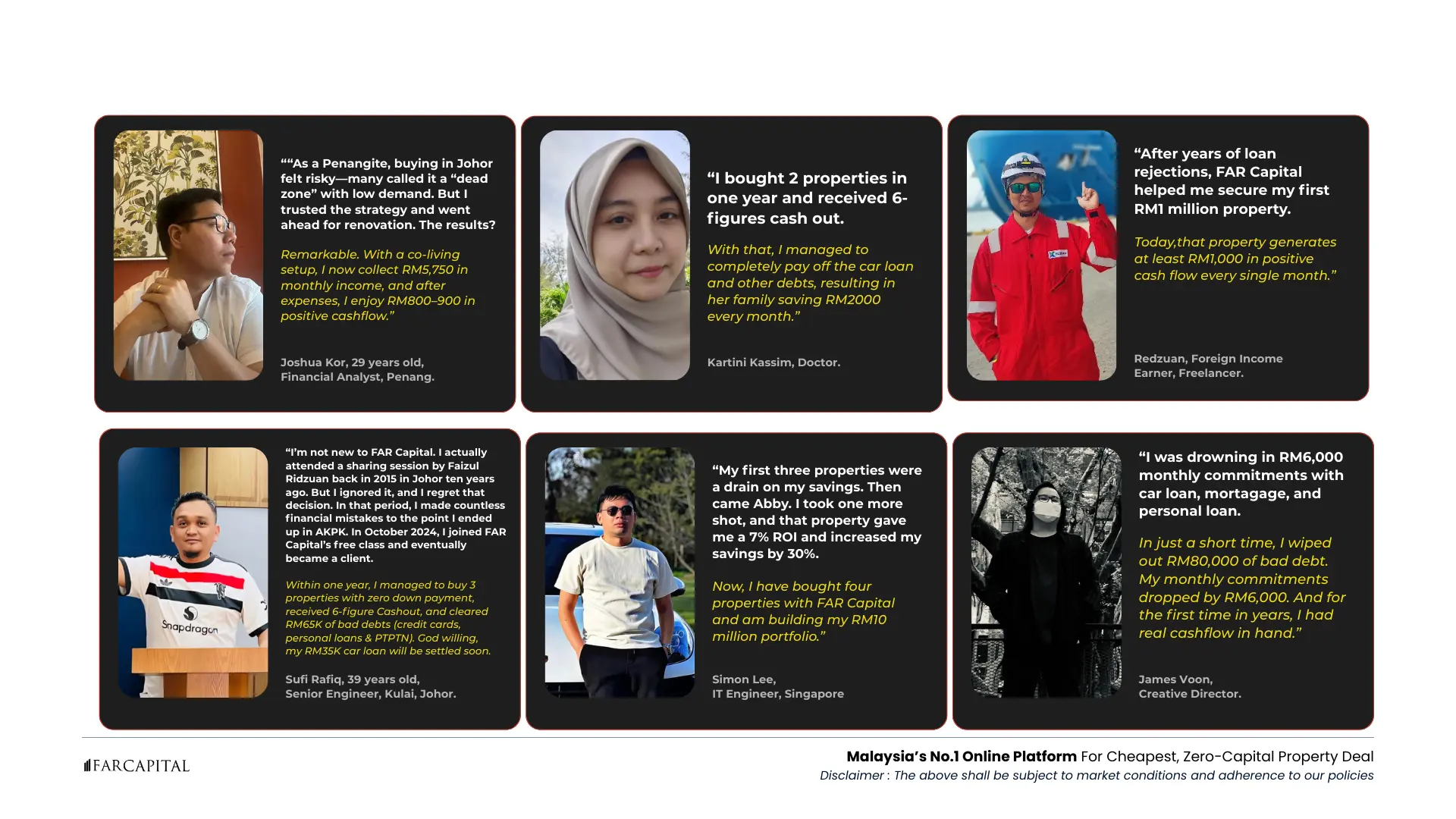

Discover the "cheat code" used by the top 10% of Malaysian property investors to build a RM1 Million portfolio even if you only have RM1,000 in starting capital.