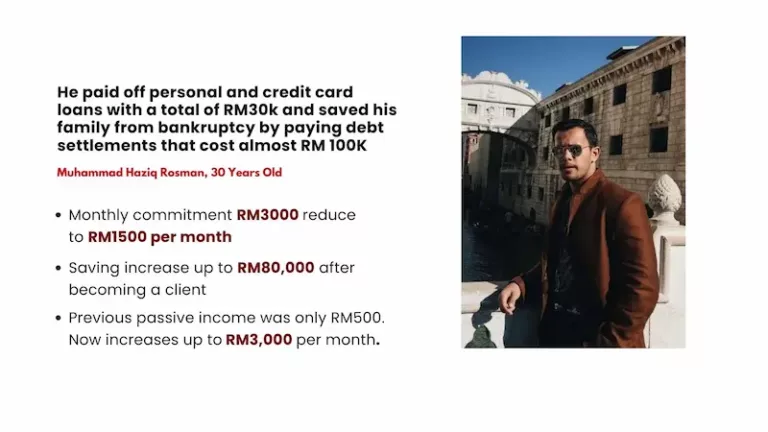

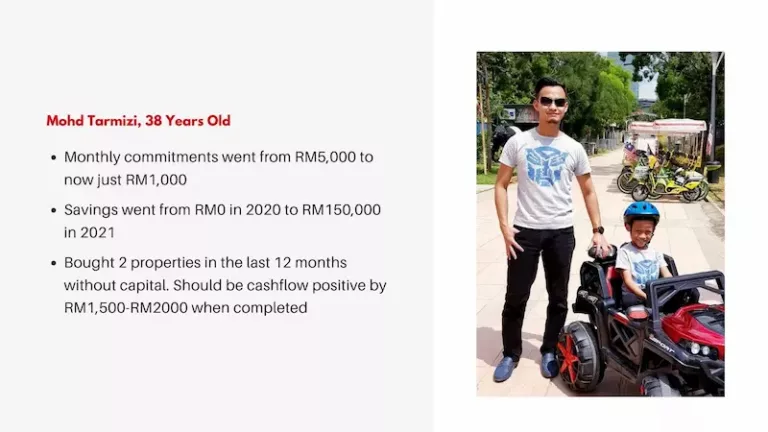

What you need to know to start slashing your debt in half within the next 12 months:

Is it really possible to reduce your monthly commitment by half in the next 12 months?

Feeling exhausted from working hard every month

Just to watch your money disappear due to loans and debts? It's frustrating, right?

Living like this can make life feel like a never-ending struggle

Living like this can make life feel like a never-ending struggle

But guess what?

There's hope! You can start cutting your debt in half within a year.