Pay the booking fee (typically RM500-RM1,000) to lock in your property choice with the developer.

Execute the Sale & Purchase Agreement and get your bank loan approved. Wait for the formal loan offer letter.

Use the i-Akaun portal to upload your stamped SPA and loan documents. Apply for Account 2 withdrawal.

EPF funds are credited directly to your bank account or to the developer, depending on your application type.

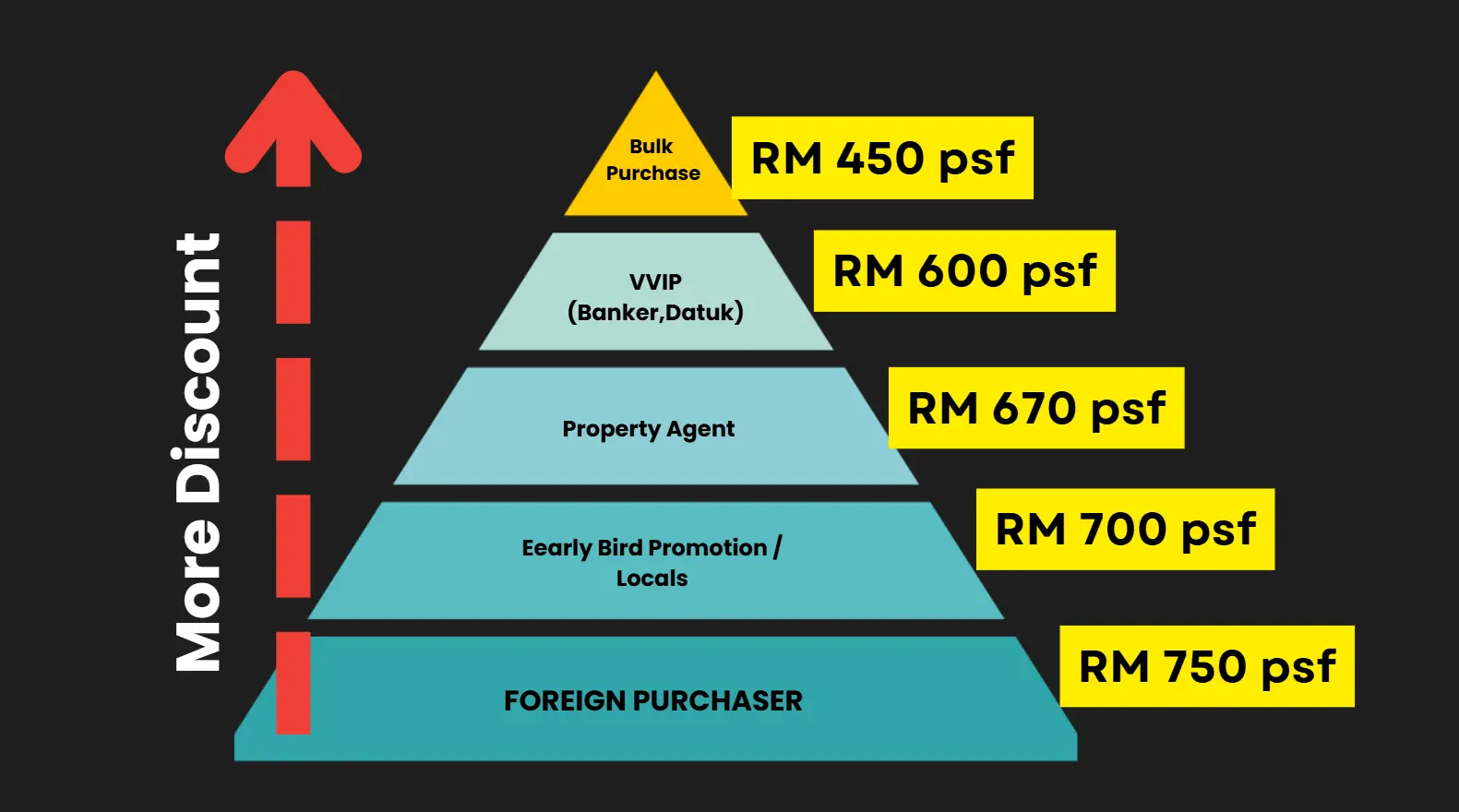

The Difference: Government schemes are a safety net; our methodology is a wealth-building engine. You may find that with our deals, you won’t even need to exhaust your government incentives to get the keys to your purchase.

Yes, zero capital investment is completely legal in Malaysia, provided all documents (SPA, Loan Agreement) accurately reflect the true purchase price. The "zero capital" aspect typically comes from developer rebates, EPF withdrawals, or cashback arrangements that are structured within legal bounds. Always ensure your developer is reputable and registered under HDA (Housing Development Act).

Yes, you can use EPF Account 2 for a second property purchase under specific conditions. You must have either sold your first property, or you are purchasing the second house for "Love & Care" purposes (for immediate family members). The property must be in Malaysia and you need to provide supporting documents to KWSP.

For property purchase, you can withdraw from EPF Account 2: (1) Up to 10% of the property price to cover down payment, plus (2) Legal and incidental fees. The withdrawal amount cannot exceed your Account 2 balance. For monthly installments reduction, you can withdraw up to 10% to reduce your loan principal.

The EPF (KWSP) withdrawal process typically takes 14-21 working days from the date of complete submission through i-Akaun. Ensure all documents (stamped SPA, loan agreement, property valuation report if required) are properly uploaded to avoid delays.

SJKP (Skim Jaminan Kredit Perumahan) is a government-guaranteed housing loan scheme designed for Malaysians without fixed income documents. This includes gig workers, freelancers, small business owners, and informal sector workers earning between RM3,000-RM10,000 monthly. It provides access to financing that traditional banks might otherwise reject.

While zero capital investment reduces upfront cash needs, you should consider: (1) Higher monthly installments due to larger loan amounts, (2) Potential negative equity if property values drop, (3) Your EPF retirement savings being reduced. Always ensure your monthly commitment is sustainable and factor in a buffer for interest rate changes.